Global 1,1,1-Trifluoroacetone Market Outlook 2026-2034: Fluorinated Intermediates Growth in Pharma & Agrochemicals

Global 1,1,1-Trifluoroacetone (CAS 421-50-1) market was valued at USD 85.4 million in 2025 and is projected to grow from USD 89.6 million in 2026 to USD 143.2 million by 2034, exhibiting a steady CAGR of 6.0% during the forecast period.

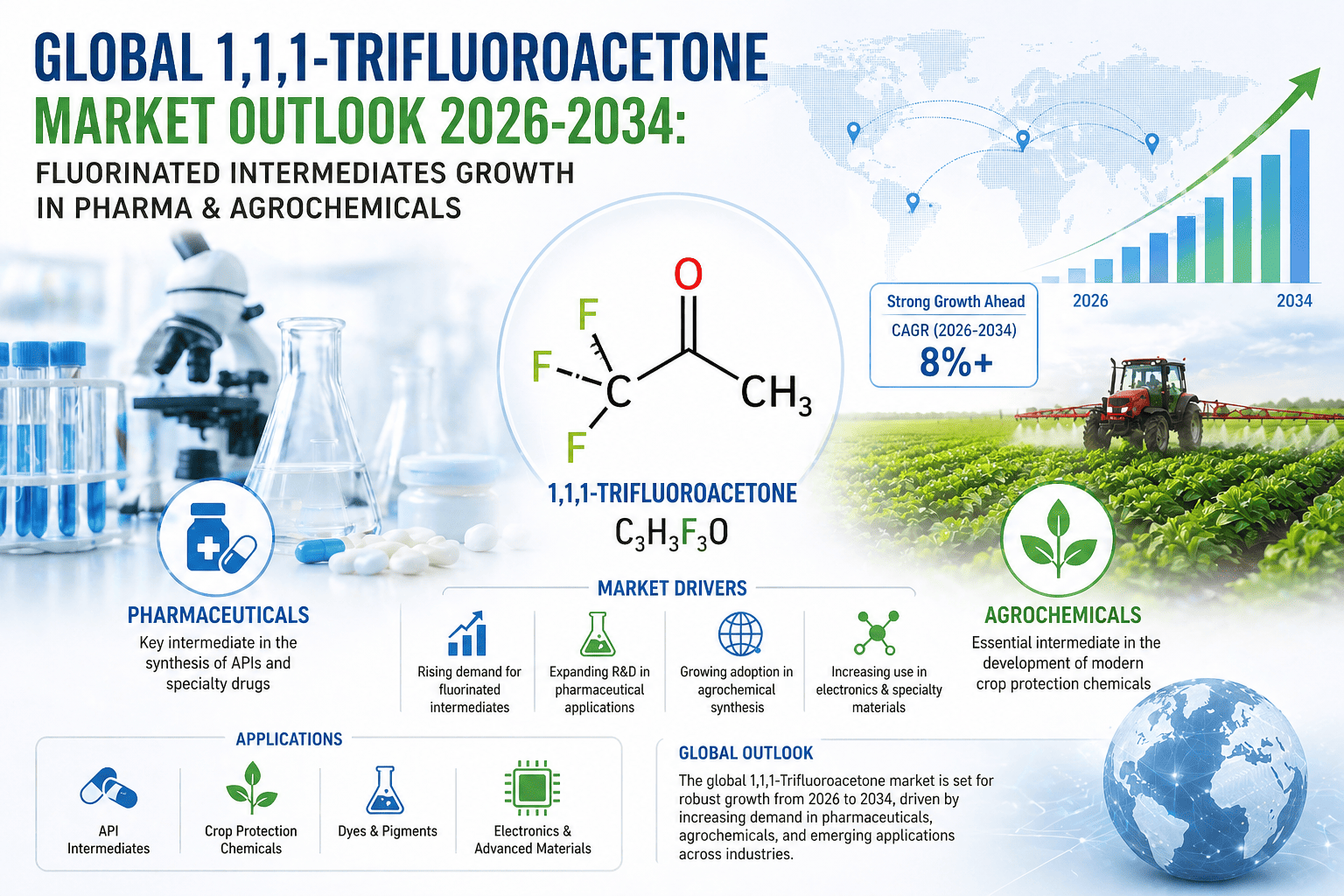

1,1,1-Trifluoroacetone, also known as trifluoromethyl methyl ketone (CAS 421-50-1), is a fluorinated organic compound with the molecular formula CF₃COCH₃. It is a colorless, volatile liquid widely utilized as a specialty chemical intermediate in the synthesis of pharmaceuticals, agrochemicals, and advanced fluorinated materials. Its distinctive trifluoromethyl group imparts unique physicochemical properties to target molecules—most notably enhanced metabolic stability, improved membrane permeability, and increased lipophilicity—making it a highly valuable building block in fine chemical manufacturing and medicinal chemistry research. While the compound has long served niche industrial purposes, its strategic importance has grown considerably as the pharmaceutical and agrochemical industries deepen their reliance on fluorine chemistry to develop next-generation active ingredients.

The market is expanding at a consistent pace, underpinned by rising demand for fluorinated intermediates across drug discovery pipelines and crop protection formulations. Growing pharmaceutical R&D activity and the increasing adoption of fluorine chemistry in active pharmaceutical ingredient (API) synthesis are central forces driving this growth forward. Furthermore, expanding agrochemical production across Asia-Pacific, particularly in China and India, continues to generate sustained upstream demand for specialty fluorinated ketones such as 1,1,1-Trifluoroacetone. Key producers operating in this space include Solvay S.A., Synquest Laboratories, and Halocarbon Products Corporation, among others.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307971/trifluoroacetone-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities waiting to be unlocked by forward-thinking industry participants.

Powerful Market Drivers Propelling Expansion

-

Rising Demand from Pharmaceutical and API Synthesis: 1,1,1-Trifluoroacetone has gained meaningful traction as a key building block in pharmaceutical synthesis, and this trend shows no sign of slowing. Its trifluoromethyl group imparts distinct physicochemical properties to target drug molecules, including enhanced metabolic stability, improved membrane permeability, and increased bioavailability—qualities that medicinal chemists actively seek when designing next-generation therapeutics. A substantial and growing share of newly approved small-molecule drugs contain at least one fluorine atom, reflecting a broader industry shift toward fluorinated compounds. The strategic importance of intermediates like 1,1,1-Trifluoroacetone continues to grow as pharmaceutical companies intensify their focus on CNS drugs, oncology agents, and antifungal compounds, all of which frequently leverage trifluoromethyl chemistry to achieve differentiated therapeutic profiles. Research activity in organofluorine chemistry has also contributed meaningfully to market demand, as academic and industrial institutions developing novel fluorination methodologies regularly utilize this compound as a direct synthetic intermediate.

-

Expansion of the Fluorochemical Industry and Specialty Chemical Applications: The global fluorochemical industry has been on a steady growth trajectory, driven by expanding applications across electronics, refrigerants, polymers, and specialty chemicals. 1,1,1-Trifluoroacetone serves as an important precursor in the production of fluorinated fine chemicals, including fluorinated alcohols, fluorinated amines, and other trifluoromethyl-containing compounds. Its relatively low molecular weight and high reactivity make it particularly versatile for chemical transformations such as condensation reactions, nucleophilic additions, and reductive aminations. Furthermore, the compound finds utility in synthesizing certain fluorinated surfactants and specialty solvents used in advanced electronic cleaning applications and surface treatment processes. The compound's role in the preparation of N-trifluoroacetyl and related protective group chemistry further broadens its utility across synthetic organic chemistry workflows, sustaining steady procurement from laboratory-scale to pilot-scale operations.

-

Agrochemical Sector Driving Volume Demand: The agrochemical industry represents a meaningful and consistently expanding demand driver for 1,1,1-Trifluoroacetone. The drive toward developing more potent, selective, and environmentally favorable crop protection molecules has intensified industry interest in fluorinated scaffolds, because the trifluoromethyl group can significantly enhance the efficacy and environmental persistence profile of herbicides, fungicides, and insecticides at lower application rates. Several classes of modern agrochemicals—including certain triazole fungicides and pyrethroids—already incorporate fluorinated moieties, and ongoing research programs at major agrochemical companies are actively exploring novel fluorinated active ingredients where intermediates like 1,1,1-Trifluoroacetone play a synthetic role. Asia-Pacific, particularly China and India, represents the most active and fast-growing agrochemical consumption region, further reinforcing the upstream demand picture for this specialty fluorinated ketone through the forecast period.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307971/trifluoroacetone-market

Significant Market Restraints Challenging Adoption

Despite its considerable promise, the 1,1,1-Trifluoroacetone market faces real hurdles that must be navigated carefully by both producers and end users to sustain long-term growth momentum.

-

High Production Costs and Raw Material Dependency: The synthesis of 1,1,1-Trifluoroacetone requires access to specialized fluorine chemistry capabilities and fluorinated raw materials, which are inherently capital-intensive to produce. Fluorspar (calcium fluoride) is the primary upstream raw material feeding the fluorochemical value chain, and its supply is geographically concentrated, with China accounting for the dominant share of global production. Price volatility in upstream fluorine-containing feedstocks, combined with the energy-intensive nature of fluorination processes, contributes to relatively high and sometimes unpredictable production costs for downstream specialty fluorochemicals including 1,1,1-Trifluoroacetone. These cost dynamics limit the compound's price competitiveness compared to non-fluorinated ketone alternatives in applications where fluorination is not strictly required, which can slow penetration into more cost-sensitive markets.

-

Availability of Alternative Trifluoromethylating Agents: The market also faces structural competitive pressure from a growing portfolio of alternative trifluoromethylation reagents and fluorinated building blocks. Compounds such as the Ruppert-Prakash reagent (trimethylsilyl trifluoromethane, TMSCF₃), Togni's reagent, and various electrophilic and radical trifluoromethylation reagents have expanded the synthetic toolkit available to medicinal and process chemists. In many synthetic contexts, these alternatives offer advantages in terms of handling safety, reaction selectivity, or functional group compatibility, which can reduce the preference for 1,1,1-Trifluoroacetone as a fluorine source or intermediate. The continued innovation in fluorination chemistry is therefore a structural restraint on the compound's market penetration, particularly in high-value pharmaceutical applications where synthetic route optimization is a priority.

Critical Market Challenges Requiring Innovation

1,1,1-Trifluoroacetone presents considerable handling challenges that can restrict its wider commercial adoption. The compound is a highly volatile liquid with a boiling point of approximately 22°C, meaning it can rapidly volatilize at ambient temperatures. This volatility, combined with its flammability and potential for generating hazardous decomposition products upon thermal degradation, necessitates specialized storage in pressurized or cryogenic containers and the use of dedicated vapor-handling infrastructure. These requirements add to the total cost of ownership for end users and can be prohibitive for smaller research facilities or chemical manufacturers without the appropriate safety infrastructure in place.

Additionally, the transport of 1,1,1-Trifluoroacetone is subject to stringent regulations under international hazardous materials frameworks, including IATA, IMDG, and ADR classifications. Its classification as a flammable liquid with a low flash point imposes packaging, labeling, and documentation requirements that increase logistics complexity and cost. Cross-border shipments, particularly for smaller lot sizes, may face delays or restrictions that affect supply chain reliability for customers in regions with limited local production capacity. The global supply base for high-purity material remains relatively concentrated, with a limited number of fluorochemical manufacturers capable of producing the compound at commercial scale with the purity specifications demanded by pharmaceutical-grade applications—creating potential vulnerability to disruptions from production outages or geopolitical factors.

Vast Market Opportunities on the Horizon

-

Growing Role in Next-Generation Agrochemical Development: The agrochemical sector's deepening commitment to fluorinated crop protection molecules creates a well-defined and expanding opportunity for 1,1,1-Trifluoroacetone. As global food security pressures mount and pest resistance to conventional chemistries continues to evolve, agrochemical companies are investing heavily in next-generation active ingredients that deliver superior efficacy at reduced application rates. Fluorinated intermediates are central to these development programs because the trifluoromethyl group reliably improves both biological potency and metabolic stability in crop protection molecules. This dynamic ensures a consistent and growing pipeline of applications for 1,1,1-Trifluoroacetone in agrochemical synthesis over the coming decade.

-

Emerging Applications in Materials Science and Advanced Polymer Chemistry: Beyond its traditional role in fine chemical synthesis, 1,1,1-Trifluoroacetone presents emerging opportunities in materials science, particularly in the development of fluorinated polymers and specialty coatings. Fluorinated ketones can serve as reactive monomers or crosslinking agents in the preparation of polymers with tailored surface energy, chemical resistance, and thermal stability characteristics. The electronics and semiconductor industries, which require materials with precise dielectric properties and exceptional chemical inertness, represent a high-value end market where specialty fluorinated compounds command premium pricing. As demand for advanced materials in electric vehicles, 5G infrastructure, and semiconductor fabrication continues to grow, the addressable market for high-purity specialty fluorochemicals including 1,1,1-Trifluoroacetone is expected to broaden meaningfully.

-

Strategic Investments and Supply Chain Partnerships as Catalysts: The market is witnessing increased strategic engagement between fluorochemical producers and end-user industries to co-develop application-specific supply chain solutions. Strategic investments by fluorochemical producers in expanding purification and handling capabilities are unlocking adjacent market segments and offering meaningful long-term revenue diversification opportunities for established suppliers. These alliances help bridge the gap between specialty chemical production and demanding end-use environments, reducing time-to-market for novel fluorinated compound applications and creating durable competitive advantages for early movers in this space.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into High Purity Grade (≥99%), Technical Grade, and Research Grade. High Purity Grade currently leads the market, driven by its critical role in pharmaceutical synthesis and advanced specialty chemical manufacturing where even trace impurities can compromise product integrity and regulatory compliance. Research Grade material maintains consistent and growing demand from academic institutions and industrial R&D laboratories exploring novel fluorinated compound synthesis pathways. Technical Grade offerings cater to broader industrial processing needs where ultra-high purity is less critical, supporting cost-sensitive manufacturing operations in agrochemical and intermediate chemical production.

By Application:

Application segments include Pharmaceutical Intermediates, Agrochemical Synthesis, Specialty Fluorochemical Production, Chemical Research & Development, and others. Pharmaceutical Intermediates stands as the leading application segment, underpinned by the compound's unique trifluoromethyl ketone functionality that enables the synthesis of biologically active fluorinated molecules. Agrochemical Synthesis represents another strategically significant application, as fluorinated compounds derived from 1,1,1-Trifluoroacetone are increasingly employed in next-generation crop protection agent development. Specialty Fluorochemical Production leverages the compound as a key building block for advanced materials, surface coatings, and performance chemicals, while Chemical Research & Development sustains steady uptake as scientists explore the compound's versatile reactivity for novel molecular design initiatives.

By End-User Industry:

The end-user landscape includes Pharmaceutical & Biotechnology Companies, Agrochemical Manufacturers, Specialty Chemical Producers, and Academic & Research Institutions. Pharmaceutical & Biotechnology Companies constitute the dominant end-user segment, reflecting the compound's growing centrality in fluorine-based drug discovery and active ingredient manufacturing. These enterprises consistently prioritize high-purity supply chains and reliable sourcing partnerships to support regulated production environments. Agrochemical Manufacturers form an increasingly important end-user base as global demand for innovative fluorinated pesticides, herbicides, and fungicides accelerates. Specialty Chemical Producers rely on 1,1,1-Trifluoroacetone as a versatile precursor to differentiated fluorinated materials serving high-performance industrial markets.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307971/trifluoroacetone-market

Competitive Landscape:

The global 1,1,1-Trifluoroacetone (CAS 421-50-1) market is characterized by a concentrated supplier base of specialized fluorochemical manufacturers, with competition driven by synthesis expertise, regulatory compliance capabilities, and supply chain reliability. The market structure reflects the high barriers to entry associated with fluorine chemistry, including specialized equipment requirements, stringent safety protocols, and the need for deep application knowledge to serve end users in pharmaceuticals, specialty materials, and chemical synthesis effectively.

Leading the competitive landscape are established multinationals such as Solvay S.A. (Belgium) and Orbia's Fluor & Energy Materials segment (formerly Mexichem Fluor, Mexico), both of which maintain broad fluorochemical portfolios and well-established global distribution networks. Central Glass Co., Ltd. of Japan is another significant manufacturer with a long track record in fluorinated intermediates and fine fluorochemicals used across pharmaceutical and agrochemical synthesis. These larger players benefit from economies of scale, integrated fluorine supply chains, and the regulatory approvals necessary to handle and ship highly hazardous fluorinated ketones internationally. Beyond the established multinationals, mid-sized and specialized fine chemical manufacturers serve niche demand segments, particularly in research-scale and custom synthesis applications. Chinese manufacturers have become notable participants in this market, with companies in Zhejiang and Jiangsu provinces expanding their fluorochemical manufacturing capabilities and increasing competitive pressure on pricing for bulk and industrial-grade material.

List of Key 1,1,1-Trifluoroacetone (CAS 421-50-1) Companies Profiled:

-

Solvay S.A. (Belgium)

-

Central Glass Co., Ltd. (Japan)

-

Sinochem Holdings Corporation (China)

-

Alfa Aesar (Thermo Fisher Scientific) (United States)

-

TCI Chemicals (Japan)

-

Zhejiang Zhongxin Fluoride Materials Co., Ltd. (China)

The competitive strategy across this market is overwhelmingly focused on maintaining synthesis quality and regulatory compliance, alongside forming strategic supply partnerships with end-user companies in pharmaceuticals and agrochemicals to co-develop validated supply chain solutions and secure long-term demand commitments.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Holds a dominant position in the global market, driven by its well-established pharmaceutical and specialty chemicals industries. The United States serves as a key hub for the research, development, and application of fluorinated intermediates, and benefits from a mature network of chemical manufacturers and contract research organizations that consistently demand high-purity fluorinated compounds. Regulatory frameworks in North America, while stringent, have encouraged the development of safer handling practices and cleaner production processes. A dense ecosystem of universities, national laboratories, and private research institutes actively investigates novel applications of trifluoromethyl chemistry, sustaining continued interest in 1,1,1-Trifluoroacetone as a versatile reagent for next-generation specialty materials and bioactive compounds.

-

Europe: Represents a significant and mature market for 1,1,1-Trifluoroacetone, underpinned by its advanced chemical industry and strong tradition in fine chemicals and pharmaceutical synthesis. Countries such as Germany, Switzerland, France, and the United Kingdom host globally recognized chemical and life sciences companies that utilize fluorinated intermediates extensively. European regulatory frameworks, particularly under REACH, impose thorough evaluation of specialty chemicals, ensuring that market participants maintain high standards of safety and environmental responsibility. The agrochemical sector contributes meaningfully to regional demand, and active academic research programs in organofluorine chemistry across European institutions support a steady pipeline of novel applications.

-

Asia-Pacific: Is emerging as the fastest-growing regional market, driven by the expansion of the pharmaceutical, agrochemical, and specialty chemicals sectors across China, Japan, South Korea, and India. China has developed considerable capabilities in fluorine chemistry manufacturing, positioning itself as both a significant producer and consumer of fluorinated intermediates. The region benefits from lower production costs, a growing pool of skilled chemical engineers, and increasing domestic demand for advanced pharmaceutical ingredients. Japan and South Korea contribute through their high-precision chemical and materials industries, while regulatory harmonization efforts are gradually aligning the compliance environment with global norms, making the region increasingly attractive for multinational fluorochemical supply chain expansion.

-

South America & Middle East and Africa: These regions currently represent smaller but gradually evolving markets. Brazil hosts a growing pharmaceutical and agrochemical industry that relies on imported specialty chemicals, and the expansion of generic drug production and crop protection chemical formulation is expected to create incremental demand over time. The Middle East and Africa region is at an earlier stage of development, though select Gulf Cooperation Council nations investing in downstream chemical manufacturing infrastructure may over time create indirect demand for specialty fluorinated reagents. The long-term potential of both regions will be shaped by continued industrialization, investment in life sciences, and the establishment of supply chain linkages with established global fluorochemical producers.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307971/trifluoroacetone-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307971/trifluoroacetone-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/